Digital turbine – Investment thesis

Digital Turbine (APPS) is a very fast growing mobile advertising platform that grows at a rapid rate on its revenue. But where it really shines is in its bottom line, where its PSE numbers rise dramatically above 100% CAGR. This is because unlike countless other fast growing stocks, Digital Turbine is actually very profitable.

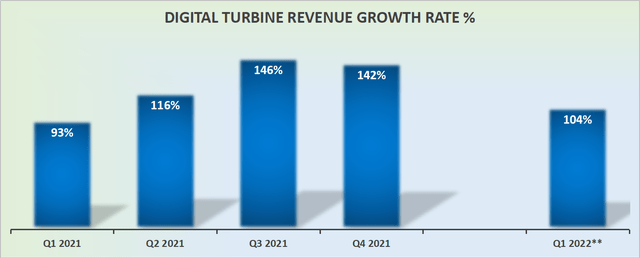

Meanwhile, investors did not like the fact that Digital Turbine’s sequential growth for the second quarter of fiscal 2022 points to just 5% organic growth, which has alarmed investors.

However, I declare that paying 5 times this year’s revenue factors is just way too pessimistic pricing. Here’s why:

Key takeaways from the Digital Turbine conference call

Before I get into the underlying dynamics of guidance, I’ll highlight the main takeaways from yesterday’s conference:

- Digital Turbine has now added more devices in the past 12 months than iPhones (AAPLs) have sold globally;

- SingleTap, Digital Turbine’s fast growing product, which is growing 600% year-on-year and is now approaching $ 100 million in revenue; about 8% of its total activity;

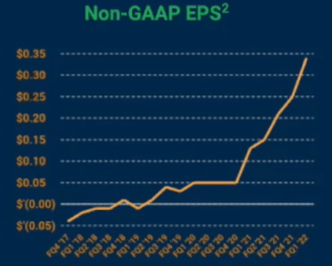

- Digital Turbine’s operational leverage results in higher EPS figures than revenue growth (CAGR EPS over 2 years of 155%)

(Source)

After 3 acquisitions, Digital Turbine’s revenues explode

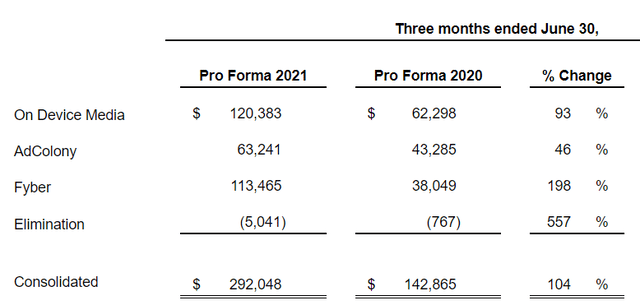

Source: author’s calculations; * Q1 2022 figure is pro forma.

A certain context is necessary, Digital Turbine reports its figure for the first quarter of 2022 as if it already owned its three acquisitions made mid-term. They also give you the numbers, as if they already owned these businesses last year.

(Source): Note that the table above does not include Appreciate separately, as it is included in the On Device Media segment.

If Digital Turbine hadn’t given you those numbers, revenue would have grown 168% year-on-year.

That said, to add to the confusion, they did not give pro forma results in their forecast for their next quarter. Investors are therefore uncertain as to what Digital Turbine’s actual targets and sustainable growth rates will be for the next quarter.

To illustrate, Digital Turbine guided $ 303 million midway through the next quarter, but that’s because they added these 3 big companies (Appreciate, Fyber, AdColony).

And compared to the same period a year ago, on the “announced” figure, at mid-term, the guidance would be up 327% year-on-year. But it’s not all organic, as they added these companies, as I noted before.

And that’s why when the company released its earnings, investors couldn’t understand how good those results actually were.

Additionally, if we take their pro forma Digital Turbine revenue of $ 292 million reported this quarter, and look at their forecast of $ 303 million next quarter, that points to 4% sequential growth, which isn’t is absolutely not in line with what investors would have hoped for. to see a mobile advertising company, in one of the strongest advertising periods.

Although I don’t invest quarter to quarter, I have been invested here for a while, I have to be frank and admit that the indications are partially confusing as this is to compare with the same period a year ago, as well as, on sequential growth. Simply put, the numbers don’t look that strong compared to other high growth ad names.

Diversification at the heart of Digital Turbine’s strategy

Keep in mind that Digital Turbine currently has three companies under its hood, which has overshadowed many of the opportunities that Digital Turbine is working on.

One of the main drivers of its future growth rates is the increase in monetization throughout the lifespan of the device compared to monetization only on first activation.

In the past, Digital Turbine technology could only serve brands by installing a few apps per new device.

But right now, while it still makes sense, other areas that Digital Turbine is moving towards are areas such as content media, the most promising of which is SingleTap, which has grown 600% in year-over-year.

SingleTap is when a consumer sees an ad on their device, taps the ad, and gets the app instantly installed on the device, without having to go to app stores. This is very important for brands as it eliminates friction and increases customer conversion up to 10 times.

One of the big concerns investors had about Digital Turbine was its reliance on a single operator and whether that operator ended up creating a competing product, whether Verizon (VZ) or another built a platform. -mobile advertising form so that it does not have to generate income. with Digital Turbine, this would significantly harm Digital Turbine’s growth prospects.

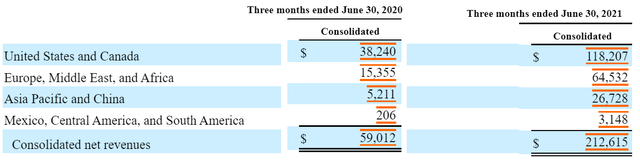

However, thanks to its acquisitions, as well as Digital Turbine’s own efforts, see below how much more diverse Digital Turbine is now compared to last year.

(Source)

The United States currently accounts for 56% of total revenue, up from 65% in the same period a year ago.

Also during the call, we learned that no customer now represents more than 10% of Digital Turbine’s pro forma revenue.

Assessment – APPS stock is still absurdly cheap

When a business grows at such a rapid pace, it’s hard to understand what’s possible over time. Right now, without a doubt, Digital Turbine will surpass $ 1.1 billion in revenue for its 2022 fiscal year. This implies that the stock is listed at almost 5 times forward sales.

(Source)

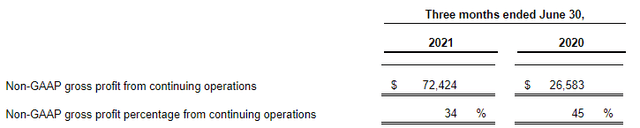

And as I expected, given that its new acquisitions are not as profitable as Digital Turbine’s core business, its gross margins have fallen from 45% last year to 34% in the current quarter.

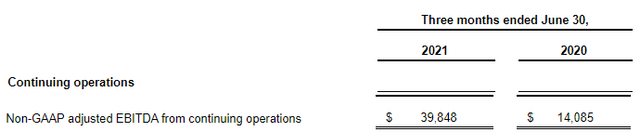

That said, as we continue to lower its income statement, we can see that, unlike other fast growing names, Digital Turbine is rapidly increasing its profitability:

(Source)

As you can see here, Digital Turbine’s EBITDA grew 172% year-on-year.

Compared to other digital ad companies, there are just not many that are priced close to 5 times revenue that show this level of growth. And that’s part of the problem for investors.

Investors are uncertain at what level Digital Turbine’s sustainable growth rates could stabilize in the medium term.

Premortem (Investment Risks)

Digital Turbine’s business model depends on a healthy mobile sales market. If the number of new devices purchased slows down, it would impact Digital Turbine’s growth prospects.

Additionally, Apple’s privacy data IDFA will continue to be a hindrance for Digital Turbine. If Digital Turbine is struggling to get enough first party data from the device, it will reduce its monetization per device and impact its growth rates.

The digital advertising market is very competitive. Not only are there countless ways for advertisers to reach consumers through social media and other platforms, Digital Turbine also has a direct competitor, ironSource (IS).

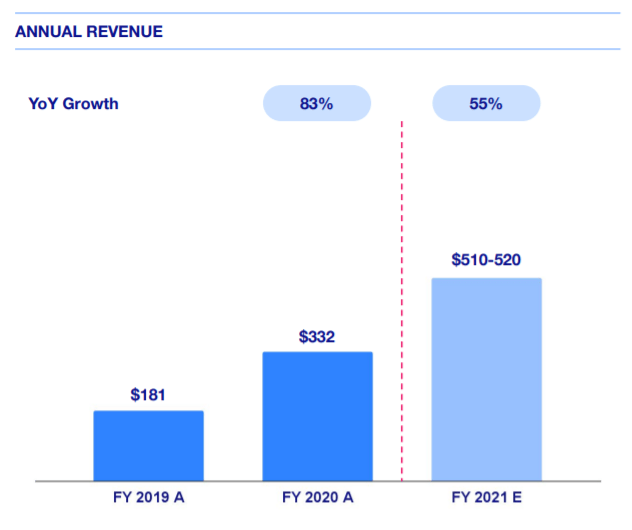

ironSource is valued at $ 11 billion and more expensive than Digital Turbine, yet ironSource’s forecast for 2021 points to less than half of Digital Turbine’s expected revenue, at $ 520 million compared to over $ 1.1 billion. dollars for Digital Turbine.

(Source)

This implies that ironSource’s price is valued at around 21 times this year’s revenue and drops to around 18 times next year’s revenue.

The bottom line

Digital Turbine is a very exciting business to be a shareholder. And there is no doubt that Digital Turbine is growing at a very rapid rate. For now, this title remains valued very cheaply at nearly 5x forward sales.

This low valuation offers investors a very large margin of safety. And given that the stock is now trading near the six-month low, I think that price is worth buying more.