What is the digital turbine used for?

Digital Turbine, Inc. (NASDAQ: APPS) provides mobile media and communications products and solutions for mobile operators, application advertisers, publishers, original equipment manufacturers (OEMs) and other third parties. The company also provides programmatic advertising and other professional products and services.

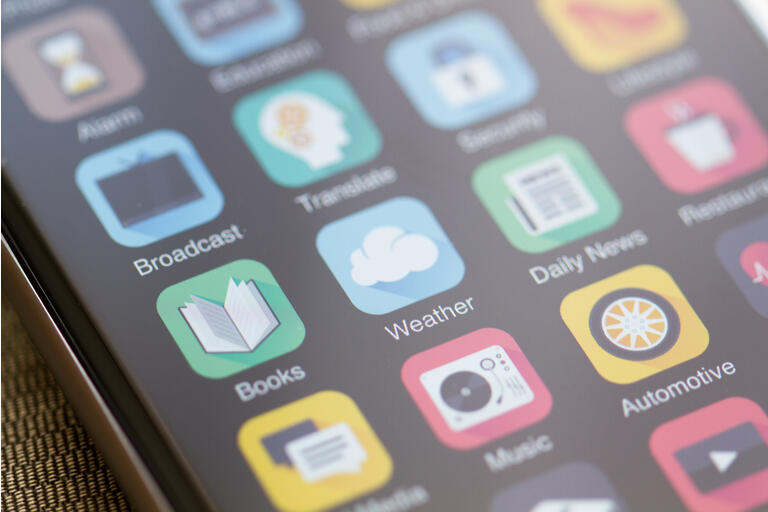

The Company has recently undergone a major change in the source of its revenues and that of its future growth. The graph below is quite informative.

Presentation graph to investors of the company.

Presentation graph to investors of the company.

The legacy business is preinstalling apps on certain phones based on demographics and other data. The software can also take user input and then preload certain applications depending on the interest. Clearly it could be lucrative as apps will pay a hefty price for this service, but the cap is limited. The software is mainly used on Android devices. These dynamic facilities are still growing, but still represent a smaller and smaller share of revenue – less than 30% when the results were last released.

The blue pie slices above are where the business can realize its potential. APPS embarked on a wave of acquisitions which immediately paid off for the results.

I now come to our recent acquisitions and our strategic game plan. With the completion of the acquisitions, we have now successfully assembled the key elements of our full-stack, end-to-end advertising technology platform. I want to spend a minute here to highlight for investors what really sets our end-to-end platform apart from other players in the industry. I should start with our overarching mission statement, which is to become the largest independent mobile advertising and monetization platform, leveraging our unique on-device technology and our long-term partner in advertising relationships. . A few years – a few words here, I want to stress, because they represent what sets us apart.

The first is to have our technology on the device, this software presence on the highlighted devices gives us distinct advantages, one of the main ones being our ability to use our patented SingleTap technology to generate significantly higher conversion rates. on the platform. Second, our independence. We have opted for vertical integration by functionality unlike many other industry players who have drifted into the content arena, thus compromising their platform neutrality and posing potential conflicts of interest for others. App publishers and advertisers on the platform. In essence, our technology presence on the device and our independent approach makes our platform more attractive to app publishers and advertisers trying to maximize monetization and ROI.

-Bill Stone, CEO on the 2022 first quarter results conference call.

Is the digital turbine profitable?

SingleTap technology, which is patented, has enormous revenue potential. This technology allows users to download apps without going through all the extra steps of using the store. For app developers, this is a huge differentiator in getting their apps to as many devices as possible. Samsung, according to Bill Stone, CEO of Digital Turbine, will launch SingleTap to the world. SingleTap accounted for approximately $ 24 million in the first quarter of fiscal 2022, compared to less than $ 2.5 million in the same quarter of fiscal 2021. The On Device Media (ODM) segment as a whole grew 104 % year-on-year (YOY) to reach over $ 120 million in the 1st quarter of fiscal 2022. The SingleTap carries a significant risk factor, and that is that Google (NASDAQ: GOOG) might become hostile to this feature because it bypasses the Google Play Store. Google might want to think twice before getting tough here, as there are several antitrust actions against the company.

Author’s Note: APPS ends March 31, therefore, the first quarter of fiscal 2022 is the period from April 1, 2021 to June 30, 2021.

With the acquisition of Fyber, the In App Media – Fyber (IAM-F) segment was created. The IAM-F segment offers a platform that enables mobile app makers to monetize their products through ad placement. Revenue in this segment is largely share-based. For example, by impression or by click. This segment delivered nearly $ 50 million in the first quarter.

With the acquisition of AdColony, the In App Media – AdColony (IAM-A) segment was created. The IAM-A segment provides, inserts and tracks advertising in applications. This segment generated $ 45 million in revenue in the first quarter. From these new segments, the Company now derives revenue from both the supply and demand of the business.

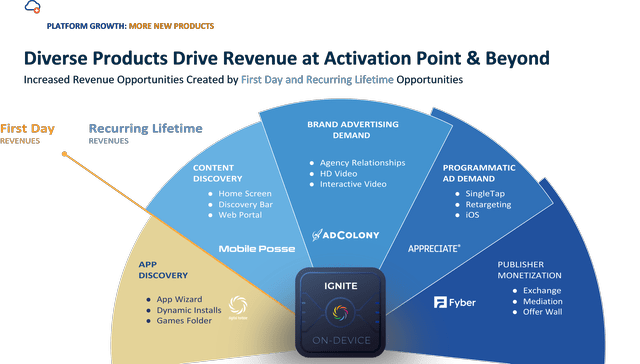

Graph created by the author with data from Seeking Alpha.

Graph created by the author with data from Seeking Alpha.

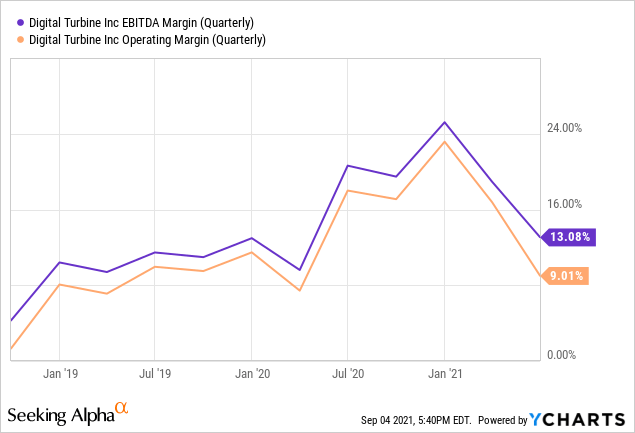

These acquisitions, along with impressive organic growth, increased revenues, operating profits and EBITDA. Operating profits and EBITDA increased 142% and 181% YOY on a 260% increase in revenue.

Acquisitions have a cost, which in this case is long-term debt. The Company went from net debt without debt to long-term debt of $ 233.8 million on June 30, 2021.

APPS share price

The stock of APPS has grown significantly over the past year, by over 164%, but has recently fallen out of favor and is down almost 30% in the past six months.

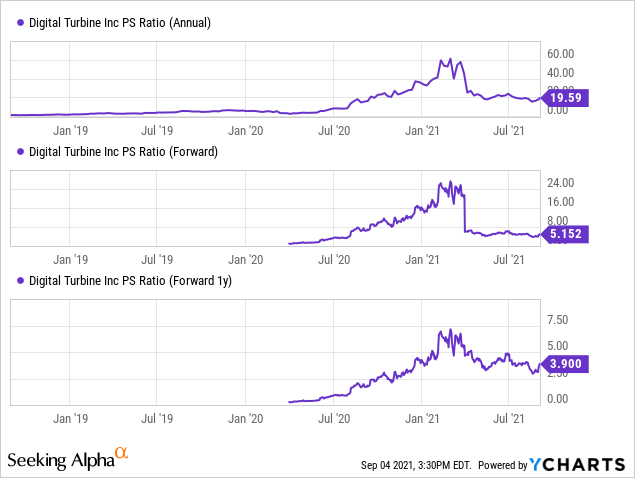

This recent weakness, coupled with improving income metrics, has made valuation metrics much more attractive. Namely, the stock is trading at just 5.15 times the forward selling price (P / S).

Is the digital turbine overvalued?

As shown below, the company’s P / S metrics on a forward-looking and one-year forward-looking basis are historically lower than at the start of 2021. It appears that investors are factoring in risk, debt and expecting to see how acquisitions are going in the future. .

The operating margin and EBITDA margin declined in the first quarter of fiscal 2022, possibly due in part to higher costs related to acquisitions. Investors should expect the latter to rebound in the coming quarters.

The stock is not significantly overvalued on the basis of growth potential, and may be quite undervalued given recent performance, provided the risks are under control and management can effectively execute the integration of acquisitions.

For the second quarter of fiscal 2022, which ends September 30, 2021, the Company forecasts revenues of $ 300 million to $ 306 million. It’s also over 42% higher than Q1 FY2022 revenue, which is pretty impressive.

Is APPS action a buy, sell or hold?

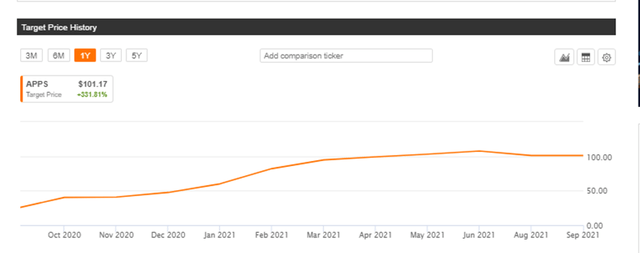

Wall Street experienced a big rebound in 2021 with constantly rising price targets. According to Seeking Alpha’s Wall Street Ratings, analysts are clear bullish with 3 ratings very bullish, 2 bullish and 1 neutral. There are no bearish odds. The average price target is now above $ 100 per share at $ 101.17. This implies a massive 58% rise from the close of 3/9/2021.

Seeking Alpha chart.

Seeking Alpha chart.

Another bullish sign is the announcement of the addition of APPS stock to the S&P MidCap 400 Index (NYSEARCA: MDY). This is positive for three main reasons.

- Credibility. A company added to an index shows its confidence in the company.

- Exposure. Being on a major index makes the stock more recognizable for individuals and institutions.

- Indexed mutual funds that track the MDY are regular buyers of the stock. This creates a basic level of demand. Unfortunately for APPS, the MDY is not a very followed index.

The signs are mostly positive for Digital Turbine and the future looks bright, but the title has fallen out of favor in recent months. It probably needs good news to return to an uptrend. The company has a chance to do so with improved earnings and margins over the next few quarters as accretive acquisitions take hold.